Digests • 14 May 2025

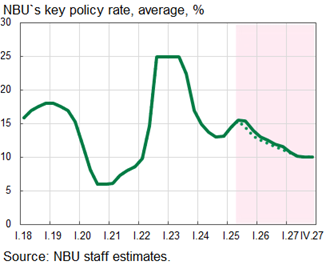

On April 17, the Board of the National Bank of Ukraine (NBU) decided to keep the key policy rate unchanged at 15.5%.

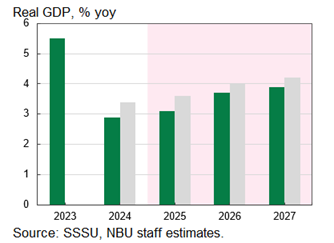

On April 24, the NBU updated its macroeconomic forecast: 2025 GDP growth was downgraded from 3.6% to 3.1%, while inflation was revised upward from 8.4% to 8.7%.

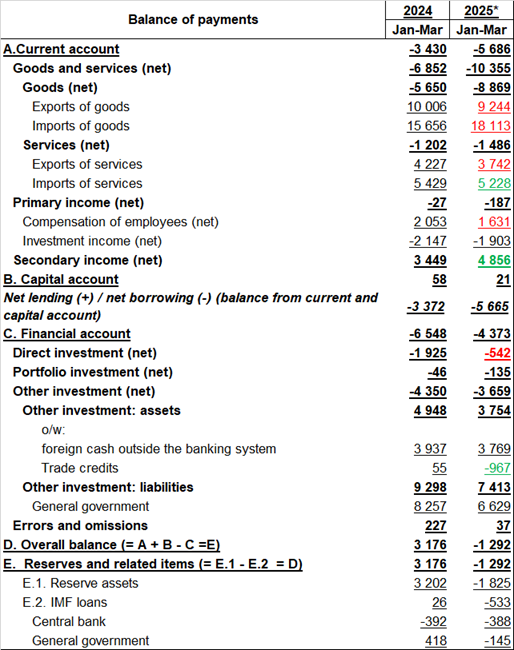

Ukraine ran a current account deficit of USD 1.4 billion in Q1 2025, compared to a surplus of USD 3.2 billion in Q1 2024. The negative balance reflects ongoing challenges in the fourth year of war.

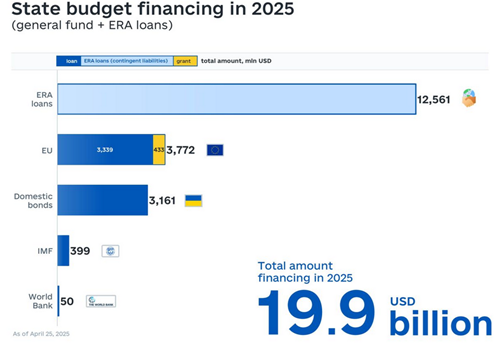

From January to April 2025, Ukraine received approximately USD 16.8 billion in external financing, including around USD 4 billion in grants, USD 5 billion more than in the same period of 2024.

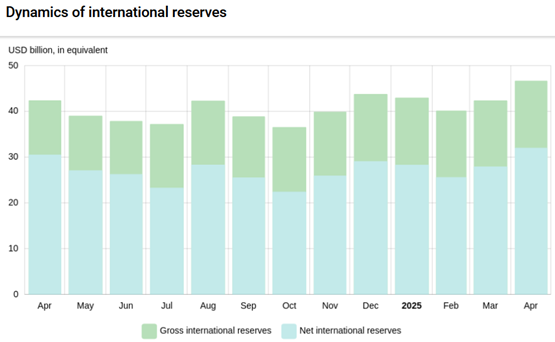

International reserves rose in April 2025 from USD 42.4 billion to USD 46.7 billion.

In its April forecast, the NBU downgraded 2025 GDP growth expectations from 3.6% to 3.1%. Growth is expected to continue, supported by improved harvests, reduced electricity shortages, and robust defense-related spending.

* Gray bars represent the previous forecast.

On April 17, the NBU left the key policy rate unchanged at 15.5%. This decision supports exchange rate stability, helps anchor inflation expectations, and contributes to disinflation toward the 5% target.

The NBU expects to maintain the current rate in the coming months, with potential for policy easing once inflation risks subside. If risks intensify, the rate could remain unchanged longer than anticipated, and the central bank stands ready to implement additional measures. The key rate is forecast to decline to 14% in Q4 2025.

According to NBU’s current macro forecast, the key rate will decrease to 14% in Q4 2025.

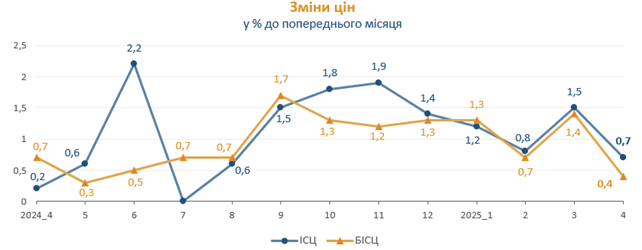

Consumer market inflation in April 2025 compared to March 2025 amounted to 0.7%, and 4.3% since the beginning of the year.

Core inflation in April 2025 compared to March 2025 amounted to 0.4%, and 3.9% since the beginning of the year.

In the consumer market in April, prices for food and non-alcoholic beverages rose by 1.8%. The highest increases were in pork and fruits, which went up by 7.9%. Prices for poultry, sugar, beef, fish and fish products, bread, lard, pasta, vegetables, and non-alcoholic beverages increased by 0.8% to 3.6%. At the same time, prices for eggs, rice, and butter decreased by 0.2% to 2.5%.

Prices for alcoholic beverages and tobacco products rose by 1.3%, primarily due to a 2.2% increase in tobacco product prices.

Transport prices fell by 0.3%, mainly due to a 2.2% decrease in fuel and lubricants. Meanwhile, passenger fares increased by 0.9% for road transport and by 0.8% for rail transport.

Price changes over the past 12 months.

Source: State Statistics Service of Ukraine.

Figure translation

Change in prices

(in % to the previous month)

2024 April May June July August September October November December 2025 January February March April

-o- CPI -A- Core CPI

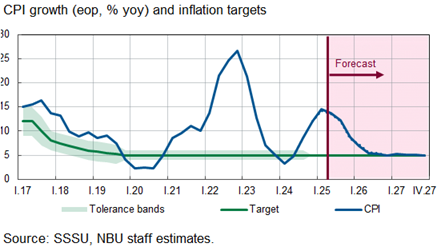

Over the past 12 months, inflation rose from 14.6% to 15.1%.

According to the NBU forecast, annual price growth will begin to slow during the summer across a wide range of goods and services. The expected increase in harvests will help reduce food inflation starting in Q3 2025 and keep it stable at a relatively low level thereafter. The decline in global oil prices, driven by international trade tensions, will also contribute to easing price pressures. As a result, the NBU projects inflation to decrease to 8.7% by the end of 2025.

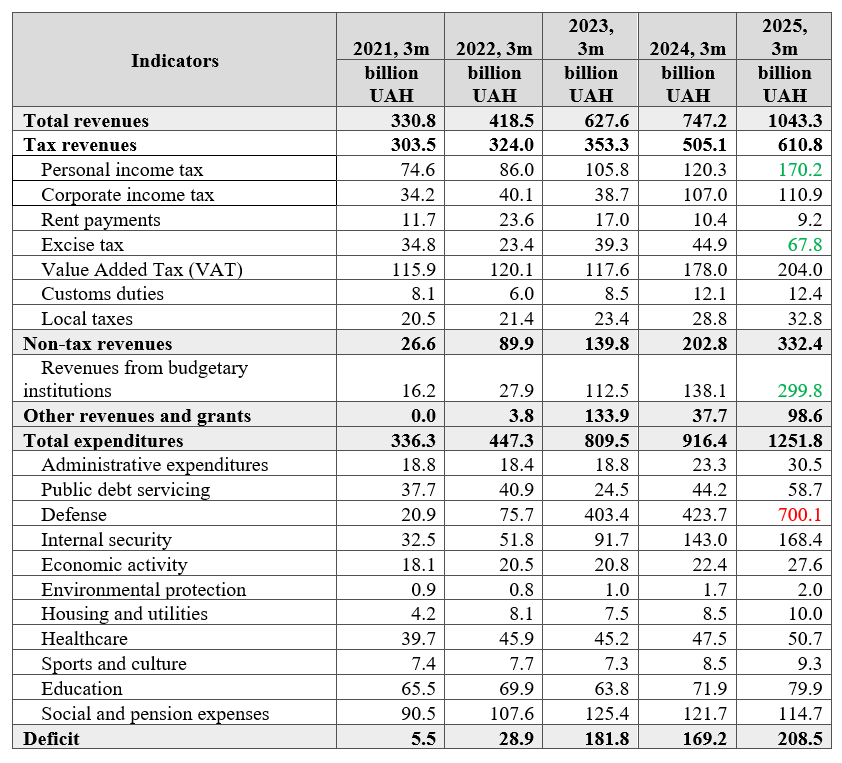

The consolidated budget for Q1 2025 closed with a deficit of UAH 208.5 billion, compared to UAH 169.2 billion in Q1 2024.

High revenues from personal income tax and increased excise collections — driven by higher military tax and excise rates on fuel and cigarettes — contributed to overall tax growth.

Defense expenditures were exceptionally high. In the first quarter, they amounted to UAH 700 billion compared to UAH 423 billion in 2024. This also reflects a higher volume of military equipment transfers to Ukraine via the budget, which was UAH 150–160 billion more than in Q1 2024.

It is also worth noting that in March, Ukraine received UAH 98 billion in grant aid (approximately USD 2.4 billion) under the ERA program.

Budget execution for Q1 2021–2025. Source: Ministry of Finance.

The state budget deficit for Q1 2025 amounted to UAH 238.5 billion, while local budgets recorded a surplus of UAH 30 billion.

In April 2025, Ukraine received external financing from several sources.

Source: Ministry of Finance

From January to April 2025, Ukraine received approximately USD 16.8 billion in external financing, of which around USD 4 billion were grants, and most of the loans were in the form of conditional credit obligations. This is significantly better than in 2024, when over the same period Ukraine received USD 11.78 billion in external financing, including USD 1.021 billion in grants and USD 10.759 billion in loans. (+USD 5 billion).

As of April 1, 2025, Ukraine’s public and publicly guaranteed debt amounted to USD 171.73 billion (+USD 2.8 billion in March 2025).

Current analysis indicates that not all loans under the ERA program are recorded as increases in public debt. In March 2025, more than USD 6 billion was received under the ERA program. Thus, it can be stated with a high degree of confidence that public debt by the end of 2025 will be lower than the IMF’s projection of 110% of GDP.

On April 24, 2025, information appeared on the Euronext exchange regarding the restructuring of GDP-linked securities, which, according to the joint position of Ukraine and the IMF, should be restructured by the end of May 2025.

According to information available through links on the Ministry of Finance website, Ukraine has proposed two options for restructuring the GDP-linked warrants.

However, creditors have not yet agreed to either proposal and have offered their own option, which was rejected by the Ministry of Finance. (75% of the 2023 growth-related payout in cash, and new bonds totaling USD 209 million).

Thus, three scenarios are currently possible:

We believe that Ukraine should eliminate the tax on its economic growth by 2041. Therefore, in our view, Option 1 proposed by the Ministry of Finance (an additional issuance of Eurobonds) is more favorable. Alternatively, under Option 2, the warrants should be bought back.

We would also like to point out that instead of a 20% debt reduction via warrants (which effectively did not occur), the Ministry of Finance is now establishing 35–36.6% in additional obligations as the baseline scenario, which in practice represents an increase in public debt. Under the first option, 2.635 * 1.35 = 3.557 billion, or an increase of USD 922 million in public debt. Under the second option, 2.635 * 0.36 = +USD 948 million increase in public debt, along with remaining payments on the warrants from 2029 to 2041.

We believe that an agreement is highly likely, but the negotiation process may prove to be challenging.

In the first quarter of 2025, the trade balance significantly deteriorated from –USD 6.85 billion to –USD 10.35 billion (–USD 3.5 billion) compared to Q1 2024. Goods exports declined by USD 750 million, and services exports fell by USD 500 million. At the same time, imports of goods increased by USD 2.5 billion. One positive aspect on the trade side was a USD 200 million decrease in services imports in Q1 2025.

Another positive development in Q1 2025 was the increase in grants to the state budget, which led to a rise in the secondary income balance from USD 3.4 billion to USD 4.8 billion.

In the financial account, a notable negative trend was the sharp drop in foreign direct investment from USD 1,925 million to USD 542 million in Q1.

Overall, Q1 2025 ended with a negative balance of payments of USD 1.4 billion, compared to a surplus of USD 3.2 billion in Q1 2024 (a decline of USD 4.6 billion). This reflects the worsening trends during the fourth year of the war.

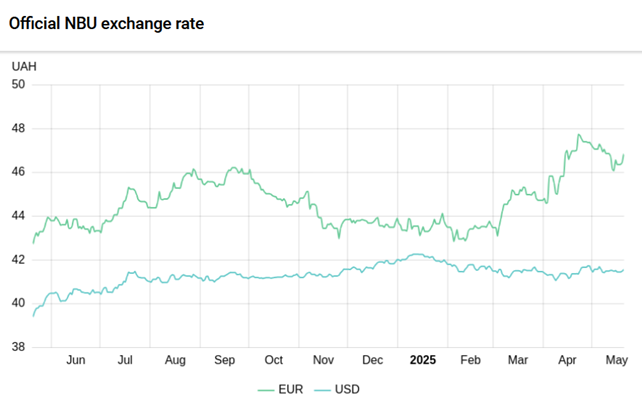

In March–April 2025, due to tariffs introduced by Trump, global currency markets experienced capital outflows from the U.S. into other currencies and gold.

EUR/USD exchange rate over the past 12 months.

The euro reached a rate of 1.15 against the U.S. dollar. This led to a sharp increase in the euro-to-hryvnia exchange rate in Ukraine, reaching 47–48 UAH per euro.

The NBU has been holding back the U.S. dollar exchange rate amid rising annual inflation. However, we must note that the hryvnia has once again begun to depreciate against the euro-dollar pair.

Hryvnia to USD and Euro exchange rate over the past 12 months. Source: NBU.

In the short term, it is difficult to forecast the euro-to-dollar exchange rate, as current dynamics are driven more by speculation than fundamentals. However, in the medium term, we expect the dollar to strengthen against the euro, as the U.S. economy remains stronger than the European one, and the Federal Reserve appears inclined to maintain its interest rate despite market and political pressure from Trump—this supports a stronger dollar.

Additionally, with growing issues in the balance of payments, we are observing a depreciation trend in the hryvnia-to-dollar exchange rate. However, we believe this depreciation will accelerate more noticeably in the second half of 2025, when inflationary pressures in the economy begin to ease.

In April 2025, international reserves increased from USD 42.4 billion to USD 46.7 billion.

Compared to March 2025, the National Bank’s net foreign currency sales declined by 17.1%. According to the NBU’s balance data, it sold USD 2,208.7 million on the foreign exchange market and purchased USD 17.5 million into reserves.

A total of USD 6,347.6 million was credited to the government’s foreign currency accounts at the National Bank, including:

Additionally, Ukraine received USD 992.0 million under the agreement between Ukraine and the United Kingdom as part of the ERA program. These funds were not included in international reserves due to their restricted (targeted) use.

A total of USD 517.9 million was spent on servicing and repaying public debt in foreign currency, including:

In addition, Ukraine paid USD 82.1 million to the International Monetary Fund.

The current volume of international reserves covers 5.6 months of future imports.

Change in international reserves over the past 12 months. Source: NBU.

Together we can change the future! Your support allows us to continue our research and provide objective analysis of key social issues. Join us today to build the future of our generations together.

Support