Digests • 19 February 2026

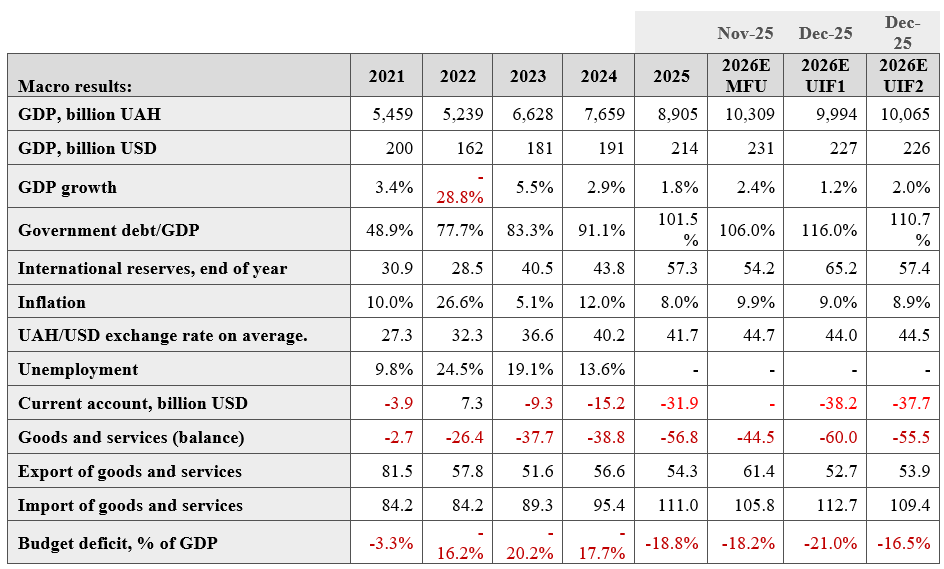

Ukraine’s public debt as of January 1, 2026, exceeded UAH 9 trillion (USD 213 billion). This exceeds 100% of GDP.

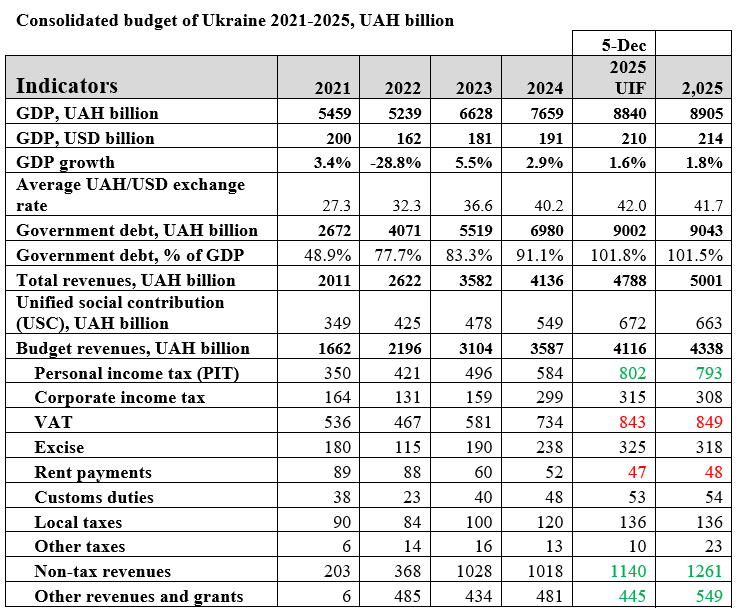

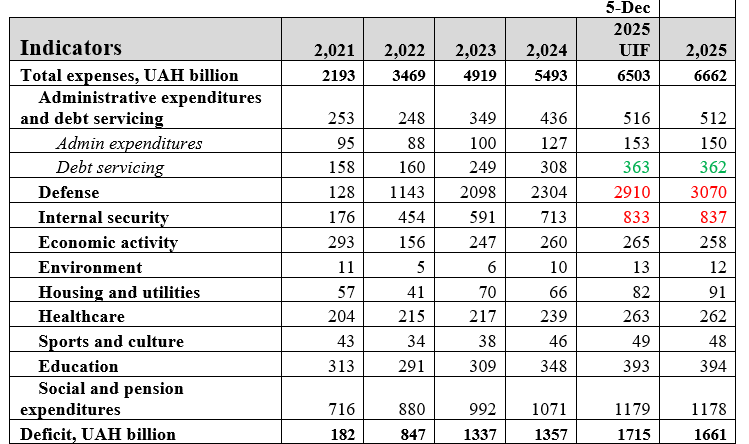

The year 2025 closed with a consolidated budget deficit of UAH 1,661 billion. Based on our current estimate, this represents 18.8% of GDP.

The trade deficit in 2025 increased from USD 38.8 billion to USD 56.8 billion (+USD 18 billion).

In the fourth quarter of 2025, Ukraine’s economic growth amounted to 3.0% of GDP.

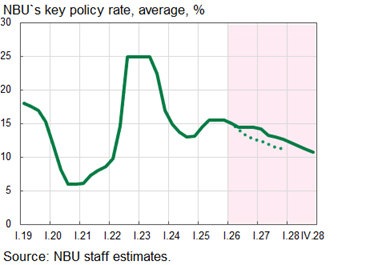

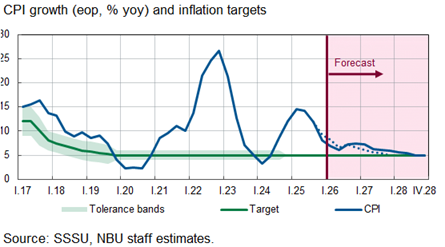

On January 30, the NBU lowered the key policy rate from 15.5% to 15.0%. On February 5, it published the new Inflation Report for Q1 2026.

International reserves increased in January 2026 from USD 57.3 billion to USD 57.7 billion.

2025E – either actual data or the NBU’s forecast for 2025.

The State Statistics Service of Ukraine estimated Ukraine’s economic growth in the fourth quarter of 2025 at 3.0% of GDP. It also revised downward the growth figure for the second quarter by 0.1% of GDP.

Source: Ukrstat.

Figure translation

Change in Real GDP

% year-on-year (compared to the corresponding quarter of the previous year)

The NBU lowered its 2025 economic growth forecast for Ukraine in its February 5 Inflation Report, from 1.9% to 1.8% of GDP.

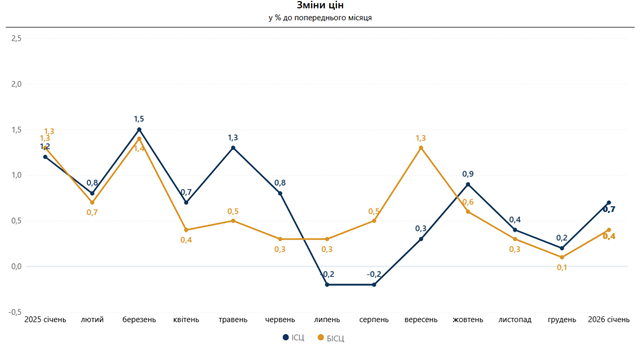

Consumer price inflation in January 2026 compared to December 2025 amounted to 0.7%, and compared to January 2025 — 7.4%.

Core inflation in January 2026 compared to December 2025 amounted to 0.4%, and compared to January 2025 — 7.0%.

Price changes over the last 12 months. Source: Ukrstat.

Figure translation

Change in prices

(in % to the previous month)

2025 January February March April May June July August September October November December 2026 January

In the consumer market in January, prices for food and non-alcoholic beverages increased by 0.8%. The largest increase (14.7%) was recorded for vegetables. Prices for grain products, fruit, fish and fish products, sunflower oil, beef, milk and dairy products, bread, and non-alcoholic beverages rose by 2.6–0.6%. At the same time, egg prices fell by 7.7%, while prices for pork, butter, poultry meat, sugar, rice, and lard decreased by 2.2–0.5%.

Prices for alcoholic beverages and tobacco products increased by 1.1%, driven by a 1.6% rise in tobacco prices.

Clothing and footwear prices declined by 4.8%, with clothing down 5.7% and footwear down 3.5%.

On January 29, the Board of the National Bank of Ukraine decided to begin a monetary policy easing cycle, taking into account the sustained decline in inflationary pressures and reduced risks related to external financing. As of January 30, 2026, the policy rate was lowered from 15.5% to 15%.

Despite inflation falling to 8% year-on-year in 2025 and the 2026 inflation forecast at 7.5%, the NBU plans to keep the policy rate at 15% throughout 2026.

Source: NBU. Inflation Report, Q1 2026.

In the new Inflation Report for Q1 2026, published on February 5, the data on the development of Ukraine’s macroeconomic indicators were updated.

The NBU lowered its forecast for Ukraine’s economic growth in 2026 from 2.0% to 1.8%.

The NBU raised its 2026 inflation forecast from 6.6% to 7.5%.

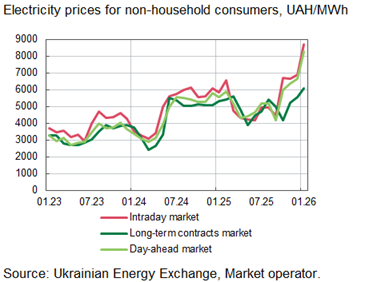

The NBU published data on the dynamics of electricity price growth for non-household consumers. In practice, over the past three years, electricity prices have tripled. In 2026, prices are expected to be even higher due to the destruction of electricity generation facilities. As a result, the Ukrainian industry appears highly uncompetitive given electricity prices that are already higher than those in Europe.

The Ministry of Finance published the results of consolidated budget execution for 2025. Data on 2025 revenues from the unified social contribution are also available, totaling UAH 662.7 billion.

In the December digest two months ago, we presented a forecast of consolidated public finances for 2025, which was very close to actual budget execution, except for several line items.

Ukraine’s consolidated budget, 2021–2025.

Key takeaways from budget execution in 2025:

The Ministry of Finance did not publish data on Ukraine’s financing in its usual format. However, data indicate that UAH 101 billion in grants was allocated to the budget in January. This is approximately USD 2.4 billion, and we believe the financing originated in the United States under the ERA mechanism.

As of January 1, 2026, balances in state and local government budget accounts totaled UAH 456 billion. Given the January grants and relatively modest January expenditures, we do not anticipate financing issues in the first quarter, while EU funding is scheduled to begin in April 2026. However, we are concerned by reports suggesting that, out of EUR 90 billion in financing planned for 2026–2027, only EUR 30 billion will be in cash, with the remaining funds allocated to weapons procurement. We believe this creates a risk of insufficient financing in 2026, particularly in the second half of the year.

In its Inflation Report, the NBU assumes that Ukraine will receive USD 51.4 billion in financing in 2026. Together with carryover balances, this should be sufficient.

As of January 1, 2026, Ukraine’s public and government-guaranteed debt exceeded USD 210 billion, reaching USD 213.22 billion (+USD 9 billion in December 2025 alone).

The increase in debt was driven by EU financing received in December 2025, the euro’s appreciation against the dollar, and the restructuring of GDP-linked warrants. The Ministry of Finance now records these as Eurobonds with a total debt of USD 3.5 billion.

In 2025, public debt increased by USD 47 billion and, according to our estimates, reached 101–102% of GDP.

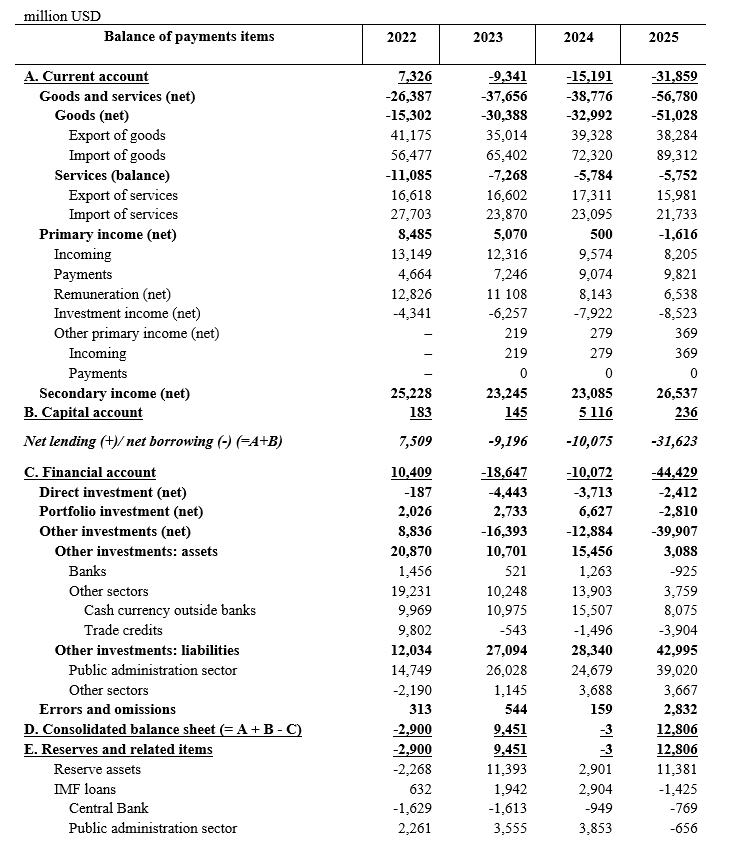

The balance of payments in 2025 was positive, driven by record financing for Ukraine. The financial account surplus increased from USD 10.0 billion to USD 44.4 billion, primarily due to rising debt from EU loans. Ukraine received USD 15 billion more in loan financing in 2025 than in 2024.

The current account in 2025 was at its lowest level on record. The deficit widened from USD -15.2 billion to USD -31.9 billion, driven by higher goods imports, which rose from USD 72.3 billion to USD 89.3 billion.

It is also worth noting the decline in remittances from Ukrainian migrant workers. In 2025, they fell to USD 6.5 billion. Before the war, they were twice as high.

Balance of payments 2022–2025. Source: NBU.

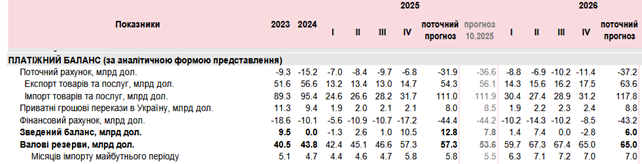

The NBU published a new balance of payments forecast for 2026.

Figure translation

INDICATORS

BALANCE OF PAYMENTS (analytical presentation)

Current account, USD bn

Exports of goods and services, USD bn

Imports of goods and services, USD bn

Private remittances to Ukraine, USD bn

Financial account, USD bn

Overall balance, USD bn

Gross reserves, USD bn

Months of future imports

(Columns: 2023, 2024, 2025 — Q1, Q2, Q3, Q4, current forecast, October 2025 forecast; 2026 — Q1, Q2, Q3, Q4, current forecast)

The NBU expects a 17% increase in exports of goods and services in 2026, from USD 54.3 billion to USD 63.6 billion, record-high imports of goods and services (rising from USD 111 billion to USD 117 billion), and international reserves of USD 65 billion by the end of 2026. We are very pessimistic about the prospects for export growth of goods and services under the current conditions of the war continuing throughout 2026.

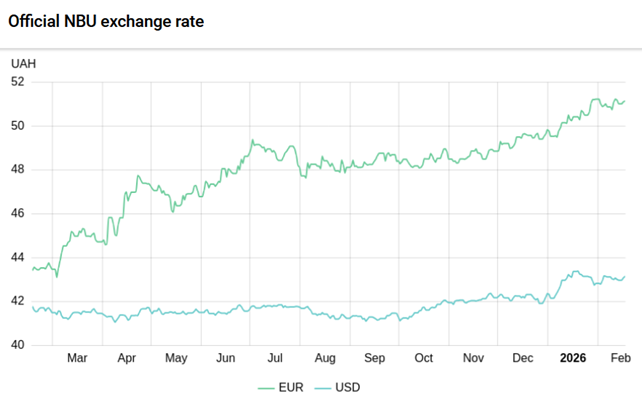

In January 2026, after maintaining the exchange rate at around UAH 42 per dollar for a full year, the NBU began a depreciation of the hryvnia, with the rate moving into the range of 43.0–43.3.

In the hryvnia/euro pair, a more pronounced depreciation was observed. This was driven by the hryvnia’s depreciation against both the dollar and the euro. On January 27, the dollar/euro exchange rate reached 1.20, pushing the hryvnia/euro exchange rate above UAH 51 per EUR.

We believe the dollar-euro exchange rate will stabilize in February. The main reason is the NBU’s forecast, which assumes more than USD 50 billion in financing for Ukraine and an increase in international reserves by the end of 2026. This suggests that the NBU expects to have sufficient foreign currency to support the exchange rate.

Hryvnia exchange rate against the US dollar and the euro over the last 12 months. Source: NBU.

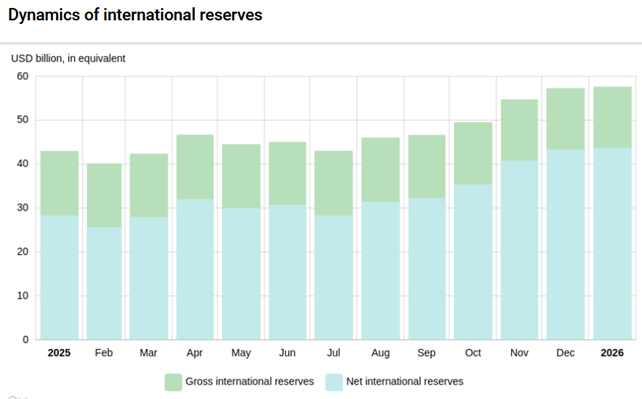

Ukraine’s international reserves as of January 2026 increased from USD 57.3 billion to USD 57.7 billion, marking a new record.

In January 2026, compared to December 2025, the National Bank’s net foreign currency sales decreased by 20.7%. According to the NBU’s balance data, the central bank sold USD 3,729.5 million on the foreign exchange market.

In January, USD 3,124.0 million was credited to the government’s foreign currency accounts at the National Bank through the World Bank’s accounts.

USD 310.7 million was paid for servicing and repayment of public debt in foreign currency, including:

USD 233.9 million — servicing and repayment of domestic government foreign currency bonds;

USD 76.8 million — payments to other creditors.

In addition, Ukraine paid USD 171.6 million to the International Monetary Fund.

The current level of international reserves covers six months of future imports.

Change in international reserves over the last 12 months. Source: NBU.

End of February 2026. Launch of a new IMF program.

This publication was created by the Ukrainian Institute of the Future with the support of the Askold and Dir Foundation, administered by ISAR Unity as part of the project “Strong Civil Society in Ukraine – a Driver of Reforms and Democracy” funded by Norway and Sweden. The content of the publication is

the responsibility of the Ukrainian Institute of the Future and does not reflect the views of the governments of Norway, Sweden, or ISAR Unity.

Together we can change the future! Your support allows us to continue our research and provide objective analysis of key social issues. Join us today to build the future of our generations together.

Support