Digests • 14 June 2025

On May 29, a staff-level agreement was reached regarding the eighth review of the Extended Fund Facility program with the International Monetary Fund (IMF).

On May 30, the Ministry of Finance of Ukraine decided not to make the payment on GDP-linked warrants amounting to USD 665 million. This constitutes a de facto default. The Ministry continues consultations to achieve a fair and comprehensive restructuring of state derivatives that ensures long-term debt sustainability without jeopardizing the country’s recovery and reconstruction.

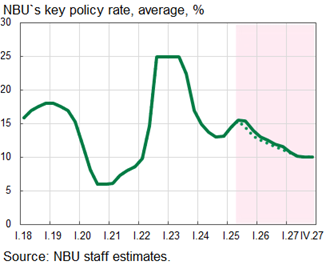

On June 5, the Board of the National Bank decided to keep the key policy rate unchanged at 15.5%.

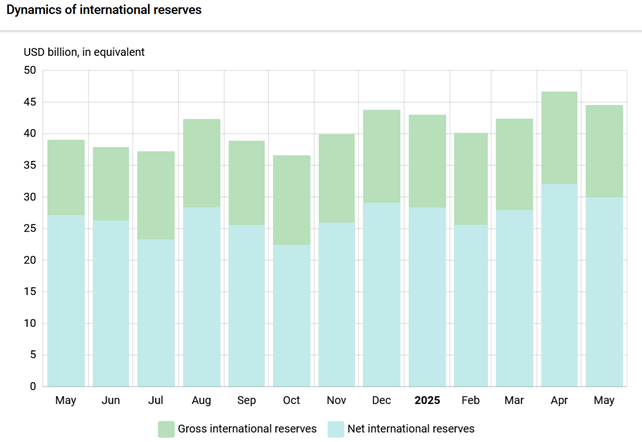

International reserves decreased from USD 46.7 billion to USD 44.5 billion in May 2025.

The International Monetary Fund (IMF) mission for the eighth review of the Extended Fund Facility (EFF) program with Ukraine, which worked in Kyiv from May 20–27, has concluded its work.

IMF representatives and Ukrainian authorities reached a Staff-Level Agreement (SLA). The agreement is subject to approval by the IMF Executive Board, which is expected to consider it in the coming weeks. Upon approval, Ukraine will gain access to SDR 0.37 billion (approximately USD 0.5 billion equivalent).

In its statement, the IMF highlighted progress in the structural reform agenda. Two structural benchmarks have been completed by the time of the eighth review, with another one expected to be fulfilled in the coming weeks. The Ukrainian side has made strong commitments to advance other key reforms.

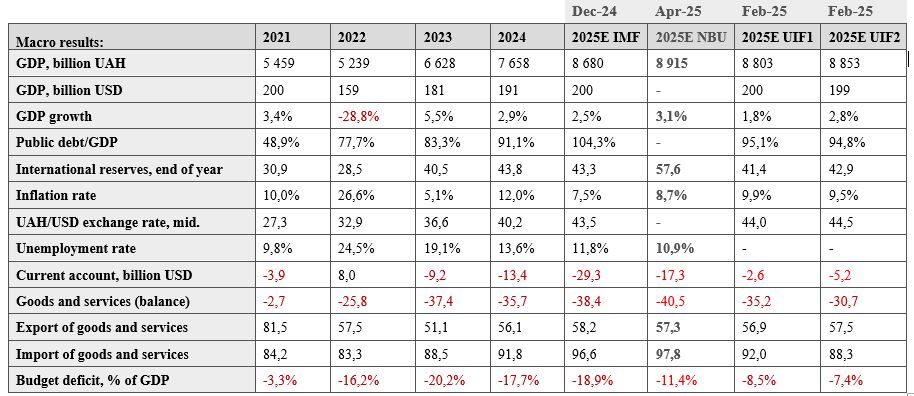

Ukraine’s economy continues to demonstrate resilience despite three years of full-scale war. The IMF expects GDP to grow by 2–3% in 2025. The inflation forecast remains unchanged. Risks to the outlook remain exceptionally high due to the uncertainty surrounding the war’s duration and prospects for peace and recovery.

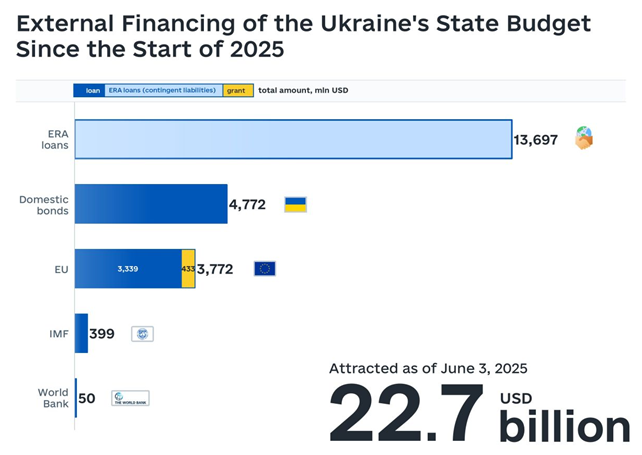

Financing the significant 2025 budget deficit will continue to require substantial external support, particularly through the ERA Loans initiative. To maintain macroeconomic stability and secure funding, it is critical to receive the full amount of the planned disbursements. Additionally, the authorities must continue efforts to mobilize domestic revenues.

On June 5, the Board of the National Bank decided to maintain the key policy rate at 15.5%. This will support currency market stability and contain inflation expectations, contributing to a sustainable disinflation path. Should threats to stable disinflation toward the 5% target intensify, the NBU will keep the rate unchanged longer than anticipated in the April macro forecast.

According to the NBU forecast, inflation will begin to decline in the summer across a broad range of goods and services, gradually moving toward the 5% target. This will be supported by the arrival of new harvests, improved energy conditions compared to last year, lower global oil prices, and reduced external price pressure, as well as the continued effect of the NBU’s monetary policy measures. A significant statistical base effect will also come from last year’s elevated regulated prices, particularly due to the one-time electricity tariff hike in June 2024.

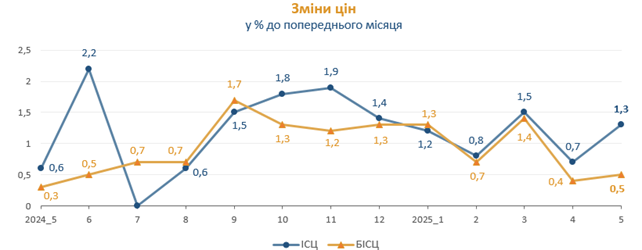

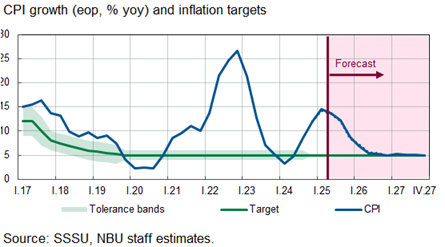

Consumer inflation in May 2025 was 1.3% compared to April 2025 and 5.6% since the beginning of the year.

Core inflation in May 2025 compared to April was 0.5%, and 4.4% since the beginning of the year.

In May, prices for food and non-alcoholic beverages in the consumer market rose by 2.8%. The largest increase was for fruits (17.6%). Prices for pork, poultry, beef, non-alcoholic beverages, fish and seafood, bread, lard, vegetables, pasta, and sugar rose by 0.7–8.3%. At the same time, egg prices dropped by 8.7%, and prices for butter, milk, and rice decreased by 0.5–0.8%.

Prices for alcoholic beverages and tobacco products rose by 1.4%, mainly due to a 2.0% increase in tobacco prices.

Clothing and footwear prices declined by 1.9%, with footwear down 2.4% and clothing down 1.5%.

Price changes over the past 12 months.

Source: State Statistics Service of Ukraine.

Over the course of 12 months, inflation increased from 15.1% to 15.9%.

According to our forecast and the NBU’s, annual inflation is expected to decline, though current data increases the likelihood of inflation exceeding 10% for the year 2025.

The consolidated budget ran a deficit of UAH 255.7 billion for the first four months of 2025, compared to UAH 264.9 billion for the same period in 2024. Revenues are UAH 437 billion higher than a year ago, while expenditures are UAH 428 billion higher.

These results are primarily due to the following factors:

As of April 2025, the state budget deficit stood at UAH 289.1 billion. Local budgets showed a surplus of UAH 33.4 billion.

In May 2025, Ukraine received external financing only from the EU under the ERA program. The fourth tranche under ERA (from income on frozen Russian assets) amounted to EUR 1 billion. For 2025, EUR 18.1 billion is planned from the EU, of which EUR 6 billion has already been secured.

Source: Ministry of Finance

As of May 1, 2025, balances on state and local government accounts totaled UAH 475 billion (over USD 11 billion). This is a new liquidity record, enabling 2–3 months of spending without external financing.

As of May 1, 2025, Ukraine’s state and state-guaranteed debt totaled USD 179.97 billion, up from USD 171.73 billion (+USD 8.24 billion in April 2025).

This increase was primarily due to large-scale financing from the ERA and Ukraine Facility programs.

Another contributing factor was the revaluation of euro-denominated debt, particularly from the EU. The euro-to-dollar exchange rate rose from 1.08 to 1.13 in April.

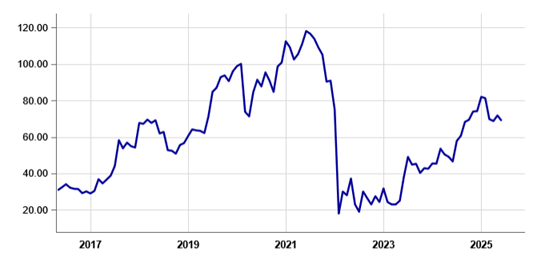

On May 30, the Ministry of Finance of Ukraine decided not to pay USD 665 million on GDP-linked warrants, which constitutes a de facto default. The Ministry continues its consultations to achieve a fair and comprehensive restructuring of public debt that ensures long-term debt sustainability without jeopardizing the country’s recovery and reconstruction.

As we noted in the previous digest, the most likely scenario was to use default as leverage to negotiate at the last moment, but this did not happen. We believe the Ministry of Finance coordinated a technical default with the IMF, but still intends to negotiate with GDP-warrant holders.

Trading prices of GDP-linked warrants on the Frankfurt Exchange. 2017–2025

As we can see, the default did not cause a significant drop in bond prices. Creditors appear to believe that restructuring terms will be agreed upon under acceptable conditions.

The Government of Ukraine failed to adopt the Budget Declaration for 2026–2028 by June 1, 2025.

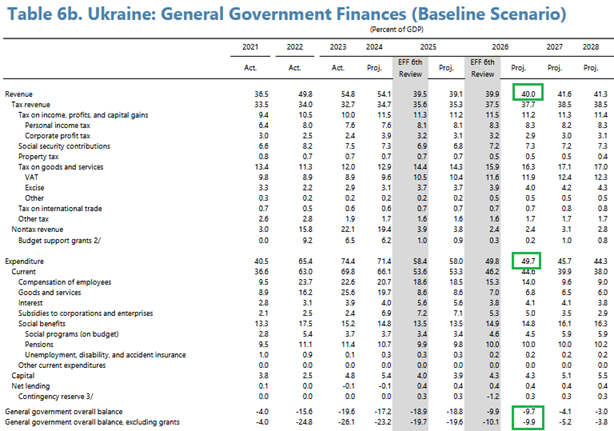

The baseline scenario for the declaration assumes the IMF forecast for 2026, which envisions the end of the war in 2025. This requires reducing the budget deficit from 18.8% to 9.7% of GDP.

IMF Base Plan March 29, 2025

However, the Ministry of Finance is preparing two versions of the Budget Declaration — one assuming the war continues through 2026 and another assuming it ends. The second version will include high defense spending and would require additional financing from the EU or other donors.

As of early June, the government’s macro table projects nominal GDP for 2026 at UAH 10.4 trillion, inflation at 9.7%, and an average exchange rate of UAH 44.8 per USD.

Projected macroeconomic indicators for budget declaration 2026–2028.

In April 2025, we continue to observe a deterioration in Ukraine’s trade balance.

For the first four months of 2025, goods exports were USD 1 billion lower than in the same period of 2024, and services exports were USD 600 million lower. Meanwhile, goods imports exceeded last year’s level by USD 3 billion, while services imports declined slightly by USD 300 million.

As a result, the trade balance for January–April 2025 worsened by USD 4.3 billion, reaching USD 13.949 billion compared to USD 9.646 billion in the same period of 2024.

A significant decline was also seen in foreign investment, dropping from USD 2,539 million to USD 701 million over four months.

On the positive side, there was a sharp decrease in foreign currency purchases by the population. In April, net purchases fell to USD 472 million, compared to USD 3.7 billion in Q1 2025.

Another positive is the substantial increase in grant aid. Net secondary income exceeded the January–April 2024 figure by USD 3 billion. Government loans in the first four months also surpassed last year’s figure by USD 3 billion.

Overall, negative trends in the real sector are being offset by even greater external financial support.

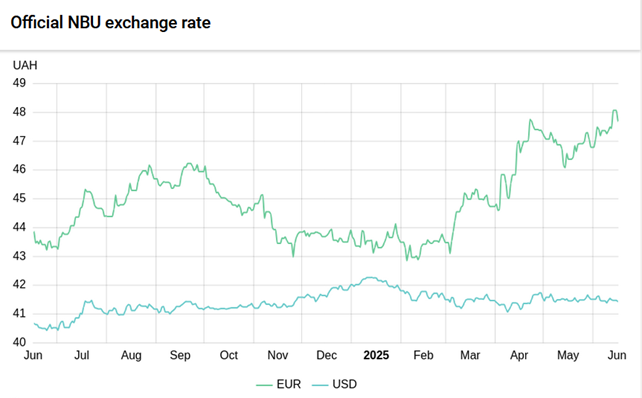

Against the backdrop of annual inflation exceeding 15%, the NBU continues to restrain inflation by preventing depreciation. However, with the euro-to-dollar rate remaining elevated, the NBU is holding the hryvnia-to-dollar exchange rate around 41.5.

Hryvnia to USD and Euro exchange rate over the past 12 months. Source: NBU.

In June, we expect the NBU to maintain its inflation-containment strategy through currency stabilization. However, starting in July, when inflation trends downward, particularly due to lower electricity prices, the NBU may shift toward a controlled devaluation of the hryvnia in light of challenges posed by the trade deficit.

International reserves declined from USD 46.6 billion to USD 44.5 billion in May 2025.

In May, the National Bank sold USD 2,962.4 million and purchased USD 1.3 million on the foreign exchange market, resulting in net sales of USD 2,961.1 million.

USD 1,357.1 million was credited to government FX accounts at the NBU in May. Of this:

Debt servicing and repayment in foreign currency amounted to USD 310.1 million, including:

Ukraine also repaid USD 296.3 million to the IMF.

Current international reserves cover 5.4 months of future imports.

Late June – Early July: IMF – 8th review with updated forecasts for Ukraine

July 10: UIF macroeconomic forecast update for 2025

Together we can change the future! Your support allows us to continue our research and provide objective analysis of key social issues. Join us today to build the future of our generations together.

Support