Digests • 06 February 2026

Monthly Energy Digest – January 2026

On January 14, parliament voted to appoint Denys Shmyhal as the first Deputy Prime Minister and Minister of Energy. Earlier, on January 13, the Rada voted to dismiss Denys Shmyhal from the position of Minister of Defense but failed to appoint him as an energy minister.

Denys Shmyhal has led Ukraine’s Ministry of Defense since July 2025, following five years as Prime Minister. Before his appointment to government, he served as head of the Ivano-Frankivsk Regional State Administration. He began his professional career in the private sector, serving in senior roles in the energy industry from 2017 to 2019, including Deputy General Director for Social Affairs at DTEK ZakhidEnergo.

After appointing Denys Shmyhal as energy minister, President Volodymyr Zelensky announced a state of emergency in Ukraine’s energy sector due to worsening energy supply caused by Russian strikes and severe weather conditions. However, there is currently no legal framework defining an emergency mode, leaving future actions under this regime uncertain. This statement was mainly intended to signal that the government would focus on tackling complex energy challenges following Russian strikes, rather than making specific management changes in the energy sector.

The President announced the government’s directives for the emergency situation: maximize cooperation with partners to secure needed equipment and support; ensure maximum deregulation of procedures for connecting backup energy equipment to networks; work toward a substantial increase in electricity imports to Ukraine, including raising price caps.

During January 2026, Ukraine’s power system experienced extreme stress due to significant capacity shortages, severe frosts, and the fallout from targeted attacks on critical infrastructure. At the start of the month, the situation remained difficult but manageable: energy workers prevented system failures despite increased demand caused by the cold snap. Cloudy weather further limited solar power plant operation, worsening shortages during daytime hours, while nuclear power plants carried the main load.

The situation worsened sharply on January 8-9 when the aggressor country launched a massive strike on Kyiv’s heat supply facilities, damaging key thermal power plants and several boiler houses. This caused about 6,000 high-rise buildings, or 50% of the capital’s housing stock, to be left without heat during severe frost, and roughly half a million subscribers lost electricity due to damage to substations. Heat supply was later restored to most homes in Kyiv, but repeated Russian attacks in January caused new waves of heat supply outages across entire districts of the city.

In the middle of the month, the power system experienced its worst crisis phase. Expected demand due to frost was 18-19 GW, but the actual system capacity, including imports, was only 12-13 GW. Output from hydroelectric, thermal, and combined heat and power plants fell to historical lows because of system disruptions. The situation was particularly severe in the north and northeast regions, where local power generation was destroyed, and damage to high-voltage lines complicated power transmission from other areas.

At the end of the month, the situation in the capital began to improve somewhat: emergency shutdowns were replaced with planned ones, although hundreds of homes still lacked reliable heat after the previous strikes.

On January 31, a major power system failure occurred, causing a cascade shutdown of high-voltage lines between the Western and Central parts of the Unified Energy System, as well as with Romania and Moldova. The system failure was caused by earlier damage from Russian shelling, which made the system extremely vulnerable, along with difficult weather conditions and increased demand amid capacity shortages. This failure required the unloading of nuclear power units. It led to a significant shortage, prompting the shutdown of critical infrastructure such as public transportation, water utilities, and boiler houses in Kyiv, Zhytomyr, Kharkiv, Odessa, and Dnipropetrovsk regions. The outage had a temporary impact on voltage levels in Moldova. By February 1, the system was gradually stabilized—most nuclear units returned to full capacity, and critical infrastructure was restored. However, the capacity shortage persisted.

In January 2026, the maximum capacity for cross-border electricity imports from European Union countries to the Ukraine-Moldova joint block increased to 2,450 MW. This increase resulted from collaboration among transmission system operators in the Eastern Europe Capacity Calculation Region (EE CCR), ENTSO-E, and the TSCnet Regional Coordination Center. It should be noted again that damage to the power transmission system from Russian strikes limits import capacity. In December, peak import capacity to Ukraine did not exceed 1.8 GW, and on most days the peak load ranged from 1.2 to 1.4 GW. However, in January, the capacity and total volume of electricity imports increased significantly.

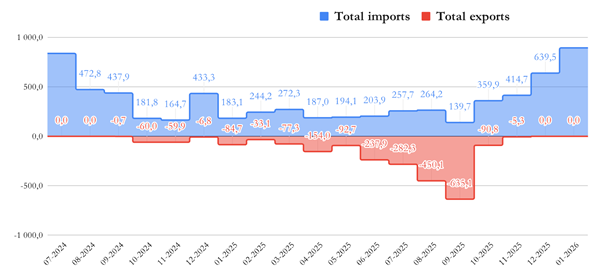

In January, Ukraine imported 894.5 MWh, marking a record volume since the country’s power system became integrated into the European network. There were no electricity exports in December. Exports were halted on November 11 due to capacity shortages in the power system.

Monthly electricity export and import volumes for the recent year

(The chart is based on ENTSO-E data)

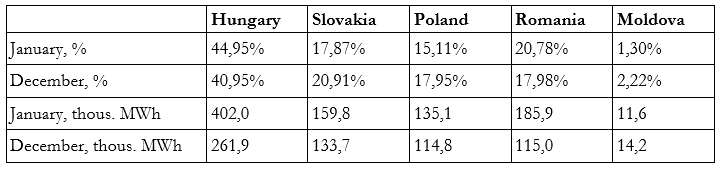

Traditionally, Hungary accounted for the largest share of imports. In general, the electricity import pattern remained nearly unchanged from previous months.

January and December import comparison

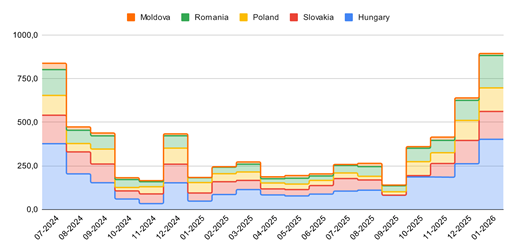

Monthly electricity import volumes by partner countries

(The chart is based on ENTSO-E data)

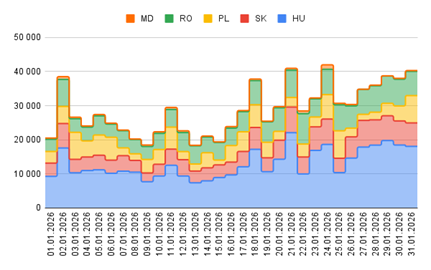

Daily volumes of electricity imports by countries of origin, MWh

(The chart is based on ENTSO-E data)

Electricity imports increased sharply in the second half of the month. Besides damage to the power grid from Russian strikes and the heightened capacity shortage, other factors also contributed to the rise in electricity imports.

Higher price caps allowed the import of more expensive electricity, boosting the total volume. The average daily import increased by 41% in the second half of the month. Additionally, in January, a record daily import of 41.9 thousand MWh was achieved. Cross-border capacity utilization rose significantly, mainly during daytime hours and evening peaks.

Another factor that boosted exports was a government directive requiring certain state-owned companies to increase electricity imports. The government required UkrZaliznytsia, Naftogaz, and UkrOboronProm to urgently secure imports to cover at least 50% of their consumption. This supports the goal of increasing electricity imports. Later, at the end of the month, Naftogaz Group reported that during the last week of January, it increased electricity imports from Europe to over 50% of the Group’s enterprises’ needs.

In 2025, the debt of balancing market participants to NPC Ukrenergo increased by 21%, reaching a record 42 billion UAH. Ukrenergo’s debt to balancing market participants increased by 36% over the year, reaching a record 22.9 billion UAH. At the end of 2024, debt to Ukrenergo was UAH 34.5 billion, and to market participants, UAH 16.1 billion.

Read a separate piece explaining the danger of increasing debts in the balancing market.

On January 16, the energy regulator increased price caps on short-term segments of the electricity market from January 17, 2026. In fact, the upper price cap for all hours in the day-ahead and intraday markets increased to 15,000.00 UAH/MWh. On the balancing market: maximum limit price – 16,000.00 UAH/MWh.

Roughly speaking, this means increasing price caps by 2 to 2,5 times during certain hours. The decision is valid until March 31, and starting from that date, the price caps will return to their previous levels. Price caps set the maximum prices for various segments of the wholesale market. As a result, this limits the import of electricity that exceeds this cap.

After reviewing the price restrictions, the BASE index on January 22 on the DAM reached a record value of 13,232.96 UAH/MWh. The weighted average price of buying and selling electricity on the day-ahead market for the first ten days of January this year was 6,622.34 UAH/MWh. According to the results of the month, this indicator amounted to 8,381.08 UAH/MWh.

On December 16, 2025, the Arbitration Tribunal of the Stockholm Chamber of Commerce Arbitration Institute issued a final decision in the case of Modus Energy International B.V. (now Green Genius International B.V.) against the State of Ukraine, fully dismissing all claims.

The investor company argued that legislative and regulatory changes in the renewable energy sector, along with payment delays by the Guaranteed Buyer, allegedly infringed on its rights and caused losses.

This is the first decision of international investment arbitration concerning disputes related to the changes introduced in 2020, particularly the reduction of feed-in tariff rates. According to the review, the tribunal found no violations of Ukraine’s international obligations. It specifically acknowledged that reforming the renewable energy support system serves a legitimate public purpose and noted that the financial claims were unsubstantiated and based on assumptions about future revenues.

The Cabinet of Ministers of Ukraine has appointed a new composition for the Supervisory Board of Energoatom based on the nomination committee’s submission. The decision is part of a reboot of the corporate governance of one of the largest strategic companies in the energy sector.

The following representatives of the state were elected to the Supervisory Board:

The approved list of independent members of Energoatom’s new Supervisory Board is as follows.

Simultaneously, appointing Patrick Fragman breaches the rules, which state that candidates should not be affiliated with companies that have contracts with Energoatom for at least one year. Nevertheless, as of January 2025, Patrick Fragman was still serving as President and CEO of Westinghouse Electric Company.

Unlike independent members, representatives of the state do not have experience in nuclear energy.

The Polish gas transmission system operator Gaz-System and the Ukrainian gas transmission system operator have agreed to increase natural gas import capacity to Ukraine starting in February 2026. From early February through the end of April, the import capacity from Poland to Ukraine will rise from 600 to 720 thousand cubic meters per hour, or from 14.4 to 17.3 million cubic meters per day. The current import capacity from Poland is 12.9 million cubic meters per day.

The expansion of available import capacities was made possible by completing the modernization of the Germanowice gas metering station.

The Polish route has remained one of the most important for Ukraine’s natural gas imports over the past year. Therefore, in 2025, Poland’s share of Ukraine’s total gas supplies exceeded 30%, with 2.1 billion cubic meters imported from Poland to Ukraine. Additionally, about 600 million cubic meters of American LNG arrived through Poland in 2025.

Ukraine has secured an extra €85 million through the European Bank for Reconstruction and Development (EBRD) instruments to increase natural gas imports. The funds will come as a grant from a European country. On January 28, the European Investment Bank (EIB) and Naftogaz of Ukraine signed another €50 million loan agreement.

Earlier, the Ministry of Economy reported a need for $100 million in natural gas imports this winter.

In 2025, Russian oil transit through Ukraine fell to a new low of 9.7 million tons.

Ukraine transported approximately 9.73 million tons of Russian oil through the southern branch of the Druzhba pipeline in 2025. Compared to last year, the volume of Russian oil transit decreased by 14% – from 11.36 to 9.73 million tons. This also marks the lowest level since at least 2014, and likely in Ukraine’s entire history since gaining independence in 1991.

According to independents assessment by ExPro Consulting agency, in 2025, Slovakia received the largest volume of Russian oil, nearly 4.9 million tons, which is a 24% increase from 2024. Meanwhile, Hungary received 4.35 million tons of oil, an 8% decline from the previous year.

The continued decrease in Russian oil transit volume results from two factors. First, the Czech Republic entirely stopped purchasing Russian oil in March, leading to the cessation of transit to the Czech Republic in early March 2025.

Second, the transit of Russian oil remained unstable throughout the year, and in some months, the volumes dropped to a decade-low level. For example, in August 2025, transit amounted to only 430 thousand tons. Ukraine carried out attacks on oil pumping stations in Russia, which affected the volume of crude oil transported from the Russian Federation to Europe.

In January, Russia attacked Ukraine’s energy infrastructure almost daily, targeting 200 facilities during the month.

On January 29, US and Ukrainian top officials informed about the achievement of a temporary energy truce between Ukraine and Russia – the parties allegedly agreed not to attack energy infrastructure. The exact terms of the truce were not publicly announced. However, on February 2, the Russians launched new strikes on Ukrainian energy facilities, which effectively violated a possible agreement.

This publication was created by the Ukrainian Institute of the Future with the support of the Askold and Dir Foundation, administered by ISAR Unity as part of the project “Strong Civil Society in Ukraine – a Driver of Reforms and Democracy” funded by Norway and Sweden. The content of the publication is

the responsibility of the Ukrainian Institute of the Future and does not reflect the views of the governments of Norway, Sweden, or ISAR Unity.

Together we can change the future! Your support allows us to continue our research and provide objective analysis of key social issues. Join us today to build the future of our generations together.

Support