Digests • 17 January 2026

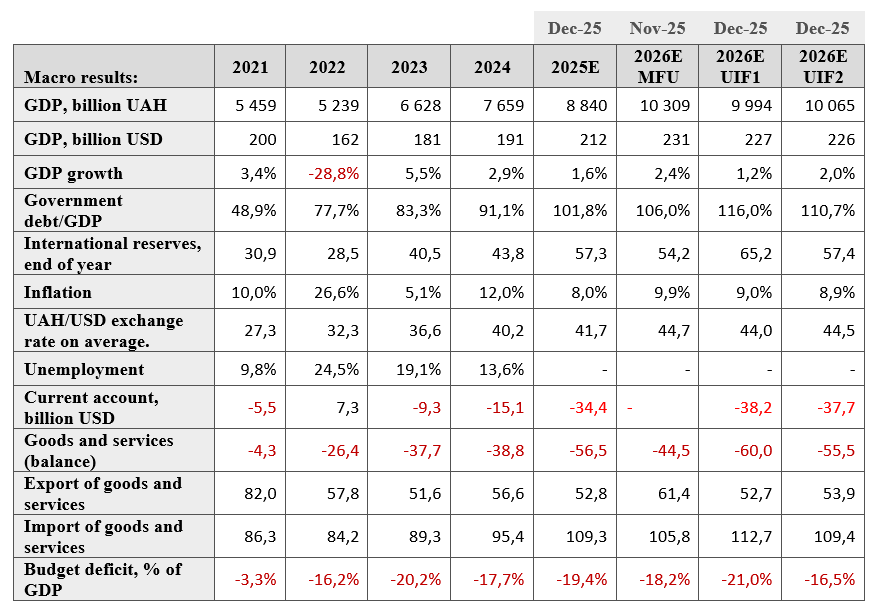

On December 22, the Ukrainian Institute for the Future released its 2026 economic forecast, available via the link. This digest also presents the key indicators from this forecast and details of the calculations.

On December 24, the Ministry of Finance announced the completion of the restructuring of GDP-linked securities (warrants). Under the restructuring terms, GDP warrants in the amount of USD 2,635,058,000 were exchanged for new Series C bonds maturing in 2032, totaling USD 3,497,665,320, as well as for Series B bonds maturing in 2030 and 2034, totaling USD 16,904,800 for each series. All GDP warrants were cancelled.

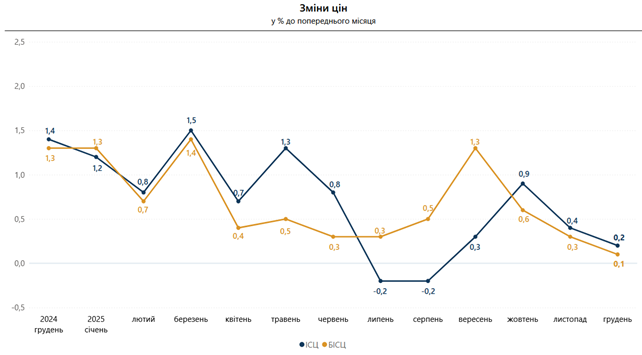

Inflation in December 2025 was 0.2%, down from 8% year over year.

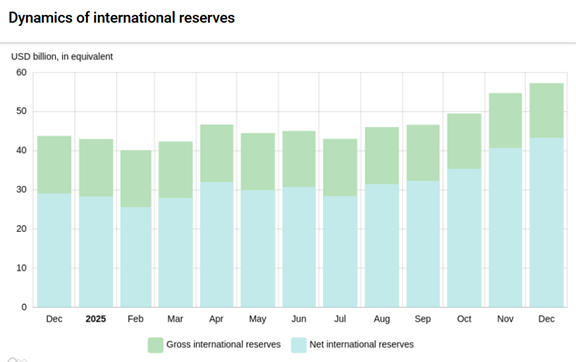

International reserves at the beginning of 2026 increased from USD 54.7 billion to USD 57.3 billion.

2025E – either actual data or the UIF forecast for 2025.

The Ukrainian Institute for the Future revised its 2025 economic growth forecast for Ukraine from 1.8% to 1.6% of GDP.

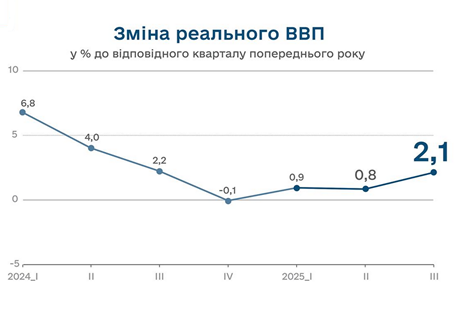

Source: Ukrstat.

Figure translation

Change in Real GDP

% year-on-year (compared to the corresponding quarter of the previous year)

In 2026, the Ukrainian Institute for the Future forecasts very moderate growth: 1.2% in the scenario of the war continuing throughout 2026 and 2.0% in the scenario of the war ending.

Nominal GDP in 2026, according to the forecast of the Ukrainian Institute for the Future, will increase to UAH 10 trillion. This is below the government’s forecast of UAH 10.3 trillion.

Consumer market inflation in December 2025, compared to November, was 0.2%, and compared to December 2024, it was 8.0%.

Core inflation in December 2025 compared to November was 0.1%, and compared to December 2024, it was 8.0%.

Price changes over the last 12 months. Source: Ukrstat.

Figure translation

Change in prices

(in % to the previous month)

2024 December 2025 January February March April May June July August September October November December

In the consumer market in December, prices for food and non-alcoholic beverages were unchanged. At the same time, prices increased by 5.6–0.7% for eggs, grain processing products, fish and fish products, bread, sunflower oil, lard, vegetables, beef, and milk. At the same time, prices decreased by 4.1–0.2% for fruits, sugar, poultry meat, pork, rice, fermented milk products, non-alcoholic beverages, and butter.

Prices for alcoholic beverages and tobacco products increased by 1.0%, which was driven by a 1.9% increase in tobacco product prices.

Clothing and footwear became cheaper by 3.9%, with footwear down 4.4% and clothing down 3.6%.

Transport prices increased by 0.7%, driven by a 1.3% rise in railway passenger transport fares and a 1.1% rise in fuel and lubricants prices.

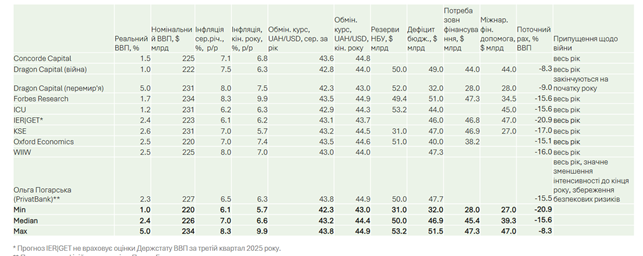

Forecasts of non-governmental organizations for 2026

In December 2025, the Centre for Economic Strategy conducted a survey of non-governmental organizations’ forecasts regarding macroeconomic indicators, the budget, and the balance of payments.

Source: https://ces.org.ua/macroforecast-2026-1/

Figure translation

Real GDP growth, %

Nominal GDP, USD billion

Inflation, avg., % y/y

Inflation, end of year, % y/y

Exchange rate, UAH/USD, avg. for the year

Exchange rate, UAH/USD, end of year

Reserves, USD billion

Budget deficit, USD billion

External financing need, USD billion

International financial assistance, USD billion

Current account balance, % of GDP

Assumptions regarding the war

Concorde Capital — war continues throughout the year

Dragon Capital (war) — entire year

Dragon Capital (ceasefire*) — ceasefire from the beginning of the year

Forbes Research — entire year

ICU — entire year

IER | GET* — entire year

KSE — entire year

Oxford Economics — entire year

WIIW — entire year

Olha Poharska (PrivatBank)** — entire year; significant reduction in intensity by the end of the year; preservation of security risks

IER | GET forecast does not take into account the State Statistics Service GDP estimate for Q3 2025.

Most non-governmental forecasts assume slow economic growth in 2026 if the war continues throughout the year, and a slowdown in inflationary processes to 6–8% in 2026. At the same time, most foresee a slight depreciation of the hryvnia in 2026, a lower need for external financing, and a decline in international reserves. For example, KSE believes that by the end of 2026, international reserves will fall from USD 55 billion to USD 31 billion amid a slight depreciation of the hryvnia.

The Ukrainian Institute for the Future’s forecast differs significantly from the presented forecasts. First, if the war continues throughout the year, this will require substantially higher external financing, leading to international reserves at the end of 2026 higher than at the beginning of 2026.

The consolidated budget for 11 months of 2025 was closed with a deficit of UAH 1,196.0 billion, compared to UAH 1,048.4 billion for 11 months of 2024.

Tax revenues in 2025 are already UAH 405.7 billion higher than in 2024.

At the same time, the state budget deficit for 11 months of 2025 totals UAH 1,245.5 billion, while local budgets’ surplus totals UAH 49.5 billion.

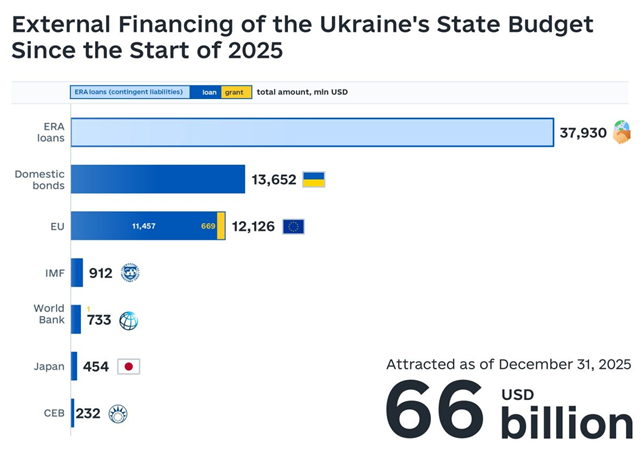

In December 2025, Ukraine received external financing from the following sources:

In total, USD 52.4 billion in external financing was received in 2025. The IMF financing plan was not fulfilled: the IMF had planned to provide a tranche in December, but the Government decided to launch a new IMF program for 2026–2029 and cancelled the loan.

Source: Ministry of Finance.

As of December 1, 2025, UAH 602 billion remained in the state and local budgets. Given that the budget received substantial Western financing and grants in December, we believe carryover balances of the state budget as of January 1 will exceed UAH 300 billion.

As of December 1, 2025, Ukraine’s state and state-guaranteed debt exceeded USD 200 billion, reaching USD 204.22 billion (+USD 7 billion in November 2025).

The increase in debt was driven by EU financing to Ukraine in November 2025 and by the euro’s appreciation against the US dollar.

Since the beginning of 2025, debt has increased by USD 38 billion over the first 11 months of 2025.

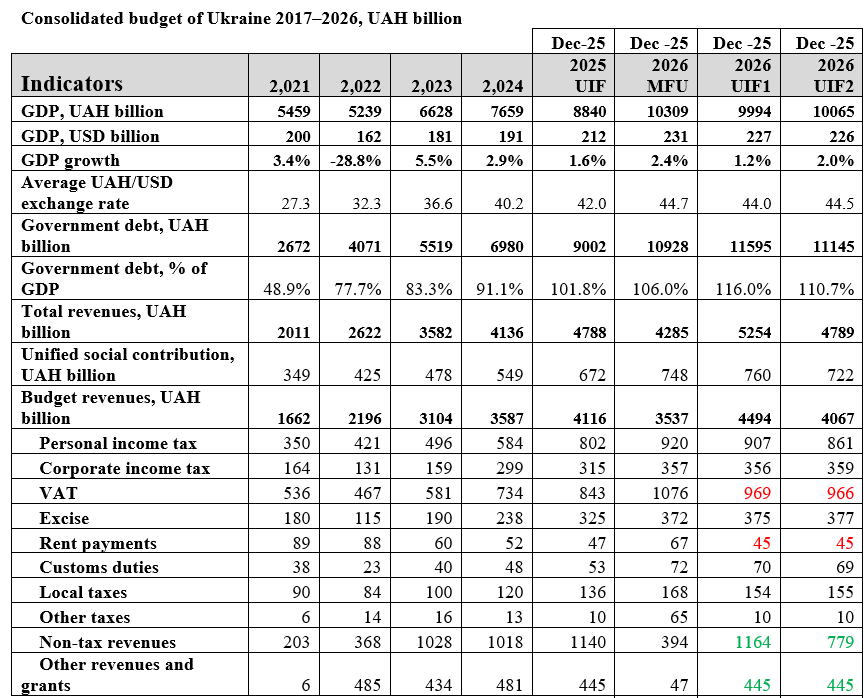

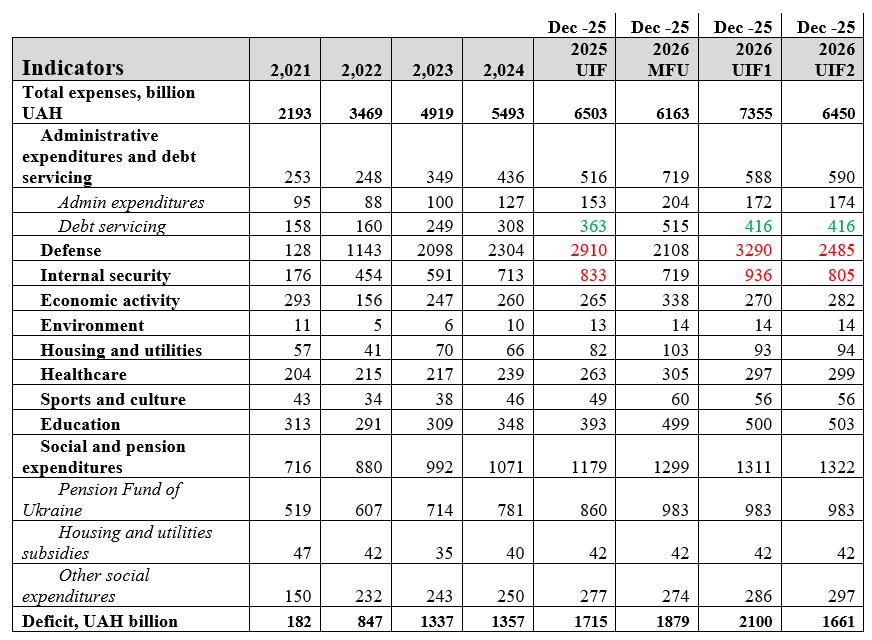

The Ukrainian Institute for the Future’s forecast of consolidated public finances for 2026 was prepared under two scenarios. The first assumes the war continues throughout 2026; the second assumes it ends in 2026.

Consolidated budget 2021–2026. Source: Ministry of Finance, UIF calculations.

The following key points regarding changes in the 2026 budget forecast should be noted.

The trade deficit continues to deteriorate. Thus, imports of goods in November reached a record level of USD 8.15 billion. At the same time, exports of goods in November amounted to USD 3.43 billion. The trade deficit in goods and services for 11 months reached a record level of USD 50.0 billion.

Overall, for 11 months, the current account balance was negative at USD -30.6 billion. This is USD 15.2 billion more than in 2024 for the same 11-month period.

The financial account, thanks to significant financing from the EU, was positive at USD 8.6 billion in November and USD 40 billion year-to-date. As a result of this financing, international reserves reached a new record at the beginning of December 2025.

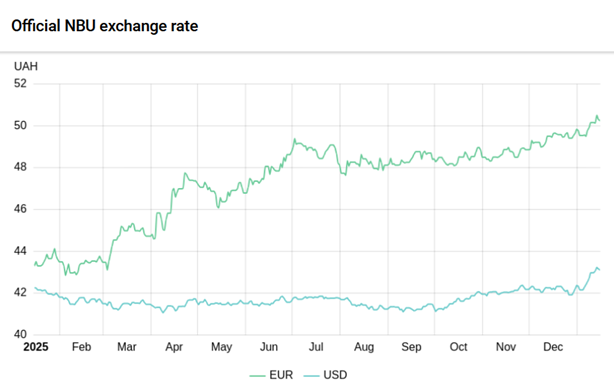

The year 2025 ended with an exchange rate of UAH 42.35 per USD. The average hryvnia-to-dollar exchange rate in 2025 amounted to 41.69. This is lower than at the beginning of 2025 (UAH 41.95 per USD).

In our December assessment, we expected the average annual exchange rate in 2025 to be around UAH 42 per USD, as we believed that the NBU, having received inflation lower than forecast, would already bring the hryvnia-to-dollar rate to UAH 43 by the end of 2025.

This did not occur in December 2025, but we are now seeing the realization of our scenario delayed: on January 8, 2026, the hryvnia-to-dollar exchange rate reached UAH 43, and the euro-to-hryvnia rate reached UAH 50 per EUR.

We believe that financing for Ukraine in 2026 will be more than sufficient, as it was in 2025. The NBU, if it so wishes, can keep the hryvnia-to-dollar exchange rate at 42–43 throughout the year, even if the trade deficit reaches USD 60 billion, which is our forecast for 2026.

However, to minimize pressure on the hryvnia exchange rate as financing for Ukraine declines, it would be logical for the NBU to pursue a policy of mild, managed depreciation against the US dollar. Therefore, our 2026 forecast assumes an average exchange rate of UAH 44 per USD and UAH 45 per USD at the end of 2026. However, we allow for the possibility that the NBU may keep the exchange rate stronger in 2026.

Hryvnia exchange rate against the US dollar and the euro over the last 12 months. Source: NBU.

International reserves in December 2025 increased from USD 54.7 billion to USD 57.3 billion. This is a new historical record for Ukraine.

According to balance-of-payments data, the National Bank sold USD 4,702.1 million on the foreign exchange market and purchased USD 0.5 million into reserves. Thus, the NBU’s net foreign-currency sales in December totaled USD 4,701.6 million, 1.7 times higher than in November. The increase in NBU foreign exchange sales interventions last month was primarily due to the traditional seasonal factor—an intensification of budget expenditures and business operations at year-end.

USD 6,915.3 million was credited to the government’s foreign currency accounts at the National Bank. Of this amount:

The Government of Ukraine paid USD 668.4 million for servicing and repayment of state debt in foreign currency, of which:

In addition, Ukraine paid USD 171.4 million to the International Monetary Fund.

The current level of international reserves covers 5.9 months of future imports.

Change in international reserves over the last 12 months. Source: NBU.

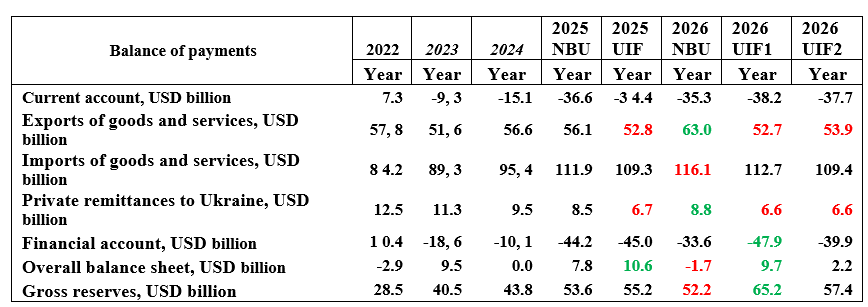

The Ukrainian Institute for the Future’s forecast of the 2026 balance of payments was prepared under two scenarios. The first assumes the war continues throughout 2026; the second assumes it ends in 2026.

Balance of payments 2022–2026. Actual 2022–2024 NBU, Forecast 2025, 2026 NBU and UIF

There are significant differences between the NBU forecast (the latest forecast is taken from the NBU Inflation Report for Q4 2025, published in October) and the UIF forecast for 2026:

January 29, 2026. NBU. Monetary policy meeting.

February 5, 2026. NBU. Inflation Report Q1 2026.

This publication was created by the Ukrainian Institute of the Future with the support of the Askold and Dir Foundation, administered by ISAR Unity as part of the project “Strong Civil Society in Ukraine – a Driver of Reforms and Democracy” funded by Norway and Sweden. The content of the publication is

the responsibility of the Ukrainian Institute of the Future and does not reflect the views of the governments of Norway, Sweden, or ISAR Unity.

Together we can change the future! Your support allows us to continue our research and provide objective analysis of key social issues. Join us today to build the future of our generations together.

Support