Stanislav Ihnatiev, Doctor of Technical Sciences, Associate Expert at the Ukrainian Institute for the Future, Professor at the Yuriн Kondratyuk Poltava Polytechnic National University

For the power sector, 2024 was a year of testing the resilience of the energy system and the courage of energy workers. Throughout the year, Russian occupiers launched 1,154 missiles targeting Ukrainian power infrastructure. The first half of 2025 brought fewer consequences in terms of destruction and damage to power facilities: electricity generation and distribution in the frontline areas of eastern Ukraine were primarily affected. As a result, energy specialists had time for partial restoration of electricity generation, transmission, and distribution facilities. In addition, Ukrainian businesses and households intensified their own projects for building distributed generation capacities to sell electricity to the grid, balance and regulate frequency within the power system, and, most importantly, meet their own needs.

This publication presents the results of an analysis of the development of distributed generation and energy storage projects in the first quarter of 2025, along with a comparison to the results of 2024.

Research methodology

The following methods of data collection, aggregation, and analysis were used in the course of this study.

Information regarding the state of the energy system, as well as destruction and damage, was derived from official statements, announcements, and publications by the Prime Minister of Ukraine, the leadership of the Ministry of Energy of Ukraine, NPC Ukrenergo, PJSC Ukrhydroenergo, PJSC Centrenergo, NNEGC Energoatom, the head and members of the National Energy and Utilities Regulatory Commission (NEURC), as well as other statistical information available in the public domain.

The location of generation facilities in temporarily occupied territories (TOT) was identified by cross-referencing energy infrastructure localization maps and TOT boundaries.

The number and localization of new distributed generation facilities were determined through:

- Analysis of reports and publications from relevant associations of electricity producers.

- Surveys of members of the Ukrainian Renewable Energy Association regarding the commissioning of new capacities.

- Interviews with engineering staff of the largest Ukrainian retailers and solar power plant installers.

- Analysis of the database of declarations on the completion of construction works by DIAM and customs declaration registries.

- Analysis of the implementation results of technical specifications for non-standard connections issued by the transmission system operator (TSO) – NPC Ukrenergo – and distribution system operators (DSOs) – regional energy companies and JSC Ukrzaliznytsia.

- Analysis of the results of auctions held by NPC Ukrenergo for the provision of ancillary services.

- Analysis of auctions for the distribution of support quotas by the State Enterprise “Guaranteed Buyer.”

- Dialogue with heads of local self-government bodies (LSGs) and homeowners’ associations (HOAs) that are installing distributed generation facilities to meet their own electricity needs.

- Surveys of representatives of state-owned companies and analysis of their tender documentation related to the purchase, installation, and connection of distributed generation equipment.

Additionally, cross-verification of collected data was carried out to prevent duplication of information regarding the commissioning of new generation capacities.

Furthermore, modeling of the territorial distribution of construction and commissioning of new distributed generation capacities was conducted using geographic information system (GIS) tools.

State of Ukraine’s energy system

Since the beginning of the full-scale invasion, 42% of Ukraine’s energy system’s generation capacity has been destroyed or occupied. The largest occupied facility is the Zaporizhzhia Nuclear Power Plant (6 GW), while the most significant losses were sustained in thermal generation, where 87% of coal-fired thermal power plants have been irreversibly lost. Additionally, 2,300 MW of hydro generation capacity have been destroyed or damaged.

Unfortunately, the enemy has not spared “green” generation either, having destroyed or occupied 3,900 MW of wind and solar power stations. Within the RES sector, wind farms have suffered less damage: available data points to fires at three wind turbines in the Donetsk and Zaporizhzhia regions, damage to a wind substation in the Kherson region, and a drone warhead strike on a wind turbine blade near the town of Ochakiv in the Mykolaiv region. In contrast, solar power stations are more vulnerable to small arms fire and missile attacks due to their large footprint and the fragility of photovoltaic modules. For example, in the Kharkiv region, all ground-based solar stations (with a total installed capacity of 28.4 MW) have been destroyed, along with most industrial rooftop PV systems (6.3 MW damaged or destroyed, and only 1.0 MW still operational); up to 1.2 GW of solar capacity is currently located in occupied territories.

From a geographical perspective, the greatest losses in generation capacity occurred in regions close to combat zones. These areas were previously energy-surplus before the attacks on the energy system and now face electricity deficits. There has also been damage to large generation facilities deep in the rear, including in Zakarpattia, Prykarpattia, and Podillia.

During the Ukraine Recovery Conference (Berlin, Federal Republic of Germany), the President of Ukraine delivered a clear message to the energy sector regarding the near-term construction of up to 1 GW of gas-fired generation. Ukrainian businesses and communities have come close to reaching this target, having built nearly 1 GW of distributed generation in 2024 and added another 1 GW in the first half of 2025. This publication will examine the structure of the distributed generation built, sources of funding, and regional distribution.

Gas generation

In the first half of 2025, state and private companies built 322 MW of cogeneration units (CGUs) connected to transmission and distribution system operators (TSOs and DSOs). Of these, 298 MW of CGUs were connected to DSO networks, enabling the formation of individual private balancing groups, most of which operate within corporate groups that also own solar and wind generation assets. Additionally, there is a growing trend of gas piston units being constructed as backup power sources but used to supply electricity to the grid when there are no electricity supply restrictions for non-household consumers (businesses).

By comparison, in 2024, Ukraine actively commissioned small thermal power plants (CHPs) and cogeneration units: 14 installations with a total capacity of 32.787 MW, including 8 units under 1 MW (with a combined capacity of 3.86 MW) and 6 units ranging from 1 to 20 MW (with a total capacity of 28.987 MW). This marked a record high since Ukraine’s independence in 1991. Furthermore, 3 small CHPs with capacities between 20–25 MW were commissioned, totaling 71.4 MW.

Local self-government bodies commissioned only 8.2 MW of gas piston generation in the first half of 2025 (compared to 128.6 MW during the same period in 2024). Most of these GPUs were installed without grid connection to ensure the operation of critical infrastructure (district heating utilities and water utilities) during emergencies. In most cases, local governments financed CGU construction from municipal budgets, whereas last year projects were largely supported by international technical assistance (ITA) programs (grants and targeted equipment provision). Unfortunately, 28.4 MW of generating equipment provided through ITA programs remains unconnected due to various reasons, particularly the lack of municipal budget resources to complete design documentation and connect to gas distribution networks.

In addition, state-owned companies based in Kyiv purchased 84 MW of CGUs. By comparison, in 2024, procurement data from the Prozorro system showed tenders totaling UAH 2.2 billion were held for divisions across Ukraine, corresponding to 37.24 MW of gas piston capacity.

It should be noted that large and medium-sized businesses (according to gas distribution companies) connected 322 MW of CGUs to DSOs in 2025, with an additional 11 MW installed without DSO connection. In 2024, 18.63 MW of gas piston units were installed without grid connection to meet internal energy needs. These were predominantly large retailers and warehouse terminals with refrigeration equipment.

Solar energy

Special attention should be given to businesses maintaining the trend of constructing solar power plants (SPPs) for self-consumption without connecting to transmission or distribution networks. In the first half of 2025, legal entities commissioned 318.4 MW of rooftop SPPs (according to DIAM registries) without grid connection, which is 1.5 times more than in the same period of 2024 (212.43 MW), and close to the figure recorded in the second half of 2024 – 384.96 MW of rooftop SPPs for self-consumption.

In addition, legal entities built 101.4 MW of grid-connected industrial SPPs. Of these, only 16 installations with a capacity of up to 1 MW are eligible for the “green” tariff, while the rest operate on the day-ahead electricity market.

According to expert estimates based on surveys of the heads of the largest companies building solar power plants for household self-consumption, 87.2 MW of such capacity were installed. It is worth noting that as of January 1, 2022, Ukraine had 1.1 GW of household solar power capacity.

It is also important to highlight that, due to the implementation of the “GreenHome” program by the State Energy Efficiency Fund and support programs from state and commercial banks extended to homeowners’ associations (HOAs), 7.6 MW of rooftop SPPs were installed on multi-apartment buildings in the first half of 2025 to cover self-consumption needs. Additionally, 1.2 MW of energy storage capacity was installed alongside.

Moreover, local self-government bodies commissioned 12.3 MW of solar power plants to meet their own energy needs. This includes 2.1 MW installed at medical institutions (1.1 MW at hospitals, 0.6 MW at outpatient clinics, and 0.4 MW at family medicine centers), 3.2 MW at educational institutions, and 6.9 MW at municipal utilities (district heating and water utilities). The majority of these projects (8.1 MW) were funded through local budgets, while 4.2 MW were implemented through international technical assistance (ITA) programs and projects.

Wind generation

In the wind energy sector, positive trends are also being observed in the commissioning of new generating capacities. According to the Wind Energy Association, 84 MW of wind power plants (WPPs) were connected to the grid in the first half of the year. By comparison, only 44.6 MW were commissioned throughout all of 2024. The record year remains 2023, with 238 MW commissioned—however, those projects had begun construction prior to the start of the war.

The most significant installations include the Skole WPP (by the company ECO-Optima in Lviv region), the first wind turbine in Zakarpattia near the town of Perechyn, and two projects developed by local agricultural enterprises near the towns of Kamianets-Podilskyi in Khmelnytskyi region and Kremenets in Ternopil region.

Electricity storage devices

A new area within distributed energy for the Ukrainian market is industrial-scale energy storage systems. These systems are now being used to address three key objectives: providing ancillary services to NPC Ukrenergo (for system balancing and frequency regulation), balancing solar power plants (SPPs) to sell electricity during peak pricing on the day-ahead market, and storing daytime solar-generated electricity for use during morning and evening demand peaks.

In the first half of 2025, 20 MW of grid-connected storage systems were commissioned. One such project is by LLC OKKO Energy in the city of Stryi (Lviv region), aimed at providing ancillary services to NPC Ukrenergo.

An additional 28.2 MW of energy storage systems were built in the first half of 2025 to meet internal consumption needs.

Bioenergy

The introduction of a permit for biomethane export has sparked a renaissance in the bioenergy sector, particularly in the construction of new biomethane plant capacities by agricultural companies. During the analysis period, a new facility was commissioned by LLC “Teofipilska Energy Company” with a capacity of 33 MW, operating on sugar factory waste (Teofipil, Khmelnytskyi region).

Thus, the total installed capacity of distributed generation in the first half of 2025 amounted to 1,021 MW (compared to 944.767 MW for all of 2024), of which 647.6 MW are connected to the electricity grid (compared to 106.374 MW in 2024).

We will now examine the geographic distribution of distributed generation projects and the correlation between short-term regional energy needs in the 2025–2030 horizon and the potential for grid connection. For visualization, the author has prepared a map (see Figure 1).

Figure 1 – Installation of Distributed Generation Capacities in 2024 (compiled by the author)

Figure translation

INSTALLATION OF DISTRIBUTED GENERATION CAPACITIES IN 2024

Total built capacities and short-term needs across regions of Ukraine

TYPE OF GENERATION | MW

- WPP (Wind Power Plants): 44.60

- SPP – Private Households: 28.58

- SPP – Grid-Connected: 10.02

- SPP – For Own Consumption: 587.22

- CGU – Grid-Connected: 32.787

- CGU – For Own Consumption: 179.633

- Mini-CHPs: 28.987

Short-term needs

Grid connection capacity

ITA (International Technical Assistance): 112.2

Business: 733.14

Local Authorities: 100.42

Legend

Total built capacities and short-term needs, MW

- more than 12

- 10–12

- 8–10

- 6–8

- 4–6

- 2–4

- less than 2

It should be noted that the analysis revealed that the geographical distribution of installed distributed generation capacities does not correlate with regional needs (primarily determined by the destruction of generating facilities) or with grid connection capabilities.

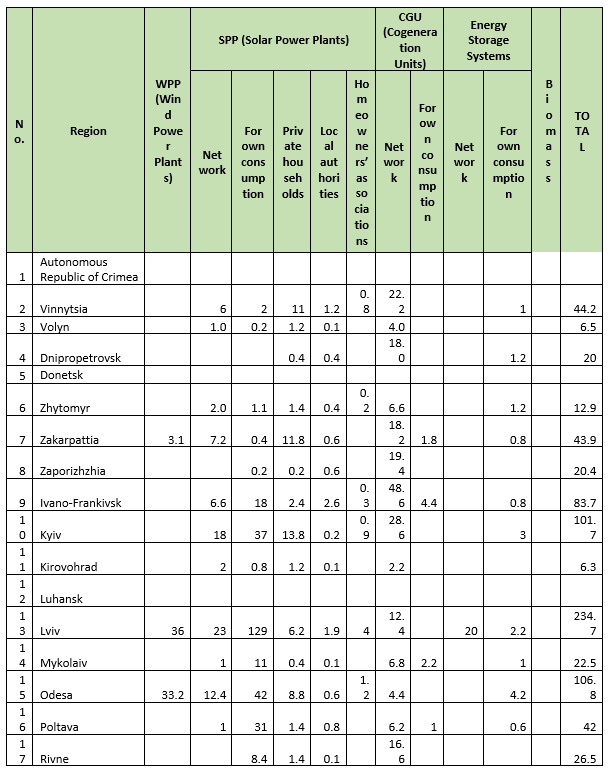

The leading region in terms of installed distributed generation capacity is Lviv region, with 234.7 MW. This includes 12.4 MW of cogeneration units built with the support of international technical assistance (ITA) programs and private businesses, 36 MW of wind capacity developed by businesses (Skole WPP), and 129 MW of rooftop solar installations on large retail and industrial facilities. Local authorities have shown limited activity due to the absence of electricity shortages, commissioning only 1.9 MW of solar power for social infrastructure. Detailed information is provided in Table 1.

The second-highest capacity was installed in Odesa region – 106.8 MW. The region is actively developing new wind projects (33.2 MW) and has built a record number (for wartime) of grid-connected ground-mounted solar power plants with a total capacity of 12.4 MW. Due to periodic local blackouts, local authorities commissioned 0.6 MW of rooftop solar power and 4.4 MW of cogeneration units.

Kyiv region, including the city of Kyiv, ranks third with 101.7 MW of distributed generation capacity built in the first half of 2025. In particular, the retail sector constructed 37 MW of rooftop solar installations for self-consumption, including supermarket chains Novus and Varus, as well as the building materials retailer Epicentr, which built Ukraine’s largest rooftop solar plant (on a single roof) with a capacity of 2.2 MW. Households in Kyiv region installed 13.8 MW of rooftop solar capacity for self-consumption, marking a national record for the first half of 2025. A more detailed regional breakdown of new capacities is presented in Figure 2.

Figure 2 – Installation of Distributed Generation Capacities in the First Half of 2025 (compiled by the author)

Figure translation

INSTALLATION OF DISTRIBUTED GENERATION CAPACITIES IN THE FIRST HALF OF 2025

Total capacity of distributed generation commissioned in the first half of 2025

Types of Distributed Generation

- WPP (Wind Power Plants)

- CGU (Cogeneration Units)

- Grid-connected

- For Own Consumption

- SPP (Solar Power Plants)

- Grid-connected

- Rooftop (Business)

- Private Households

- Local Authorities (LSG)

- Homeowners’ Associations (HOA)

- Energy Storage Systems

- Grid-connected

- For Own Consumption

- Biomass

Business: 918.2

Individuals: 90.8

Local Authorities (LSG): 8.1

International Technical Assistance (ITA): 4.2

Legend

Total installed distributed generation capacity, MW

- more than 125

- 100–125

- 75–100

- 50–75

- 25–50

- 10–25

- less than 10

In fourth place is the Ivano-Frankivsk region, with 83.7 MW of distributed generation capacity installed in the first half of 2025. The region has constructed 6.6 MW of grid-connected industrial solar power plants and 18 MW of solar capacity for self-consumption—both in the Bukovel tourist cluster and on industrial and warehouse rooftops in Ivano-Frankivsk, Kolomyia, Kalush, and Dolyna. Additionally, 48.6 MW of grid-connected cogeneration units (CGUs) and 4.4 MW of CGUs for self-consumption were commissioned, primarily by companies in the oil and gas sector.

In fifth place is Khmelnytskyi region, with 79.3 MW of distributed generation capacity installed, including the country’s largest biomethane plant (33 MW), 6.2 MW of commercial grid-connected solar power, and 8.6 MW of CGUs at municipal utilities in the cities of Khmelnytskyi, Kamianets-Podilskyi, and Starokostiantyniv. Additionally, in the first half of 2025, the Kamianets-Podilskyi wind power plant was commissioned, built from three refurbished wind turbines, with its grid connection process taking 2.5 years.

However, despite the 1,021 MW of distributed generation facilities commissioned by businesses, households, and local governments in the first half of 2025—and the 944.76 MW commissioned in 2024—a capacity gap remains. Between 2025 and 2030, there is still a need for 2,742.7 MW (2.7 GW) of additional distributed generation, while the existing electrical grid can accommodate only 2,323.4 MW of installed capacity.

Table 1 – Installed Capacities of Distributed Generation in the First Half of 2025 (compiled by the author)